Tax Day 2026: How Your Taxes Affect Your Auto Insurance

Tax Day 2026 falls on April 15, and if you’re like most of us, you’re probably thinking more about what you owe the IRS than about your car insurance. But it turns out these two topics are more connected than they seem.

Let me be upfront: for most people, personal auto insurance isn’t tax deductible. If you only use your car to commute to work, take the kids to school, and run errands, the IRS won’t give you a break. But there are important exceptions that might apply to your situation. And even if you don’t qualify for deductions, there are smart ways to use your tax refund to reduce what you pay for coverage.

Let’s see what applies to you.

When you CAN deduct your auto insurance

Here’s the truth: car insurance is only deductible if you use your vehicle for business purposes. And no, commuting to the office doesn’t count as “business use” according to the IRS.

If you’re self-employed or own a business

This is the most common situation where auto insurance becomes deductible. If you drive to visit clients, deliver products, attend work meetings, or any other activity directly related to your business, you can deduct a portion of your insurance.

The key is separating personal use from business use. If you use your car 60% for work and 40% for personal stuff, you can only deduct 60% of your insurance premium.

If you drive for Uber, Lyft, DoorDash or similar services

Good news if you do deliveries or rideshare: your auto insurance qualifies as a business expense. All the time you spend with the app on waiting for passengers or deliveries counts as commercial use.

That said, you need to keep track of your miles. The IRS is very specific about this.

Two ways to calculate your deduction

The IRS gives you two options for calculating how much you can deduct for vehicle use in 2026:

The first is the actual expenses method. You add up everything you spend on your car (gas, maintenance, insurance, repairs, depreciation) and apply your business use percentage. If you spent $6,000 total and used the car 70% for business, you can deduct $4,200.

The second option is the standard mileage rate. For 2026, the IRS set it at 72.5 cents per mile. You multiply your business miles by this amount and you’re done. This method is simpler because you don’t have to keep all the receipts, just a mileage log.

My advice: calculate your deduction using both methods and choose whichever gives you more. There’s no penalty for picking one over the other.

When you CANNOT deduct your auto insurance

Let’s be clear: if you’re a regular employee of a company and only use your car to get to work, your insurance isn’t deductible. The Tax Cuts and Jobs Act of 2017 eliminated this possibility for most employees.

It also doesn’t apply if your employer already reimburses you for vehicle use. You can’t receive reimbursement AND take the deduction.

And of course, purely personal use (going to the gym, vacations, taking kids to soccer) is never deductible.

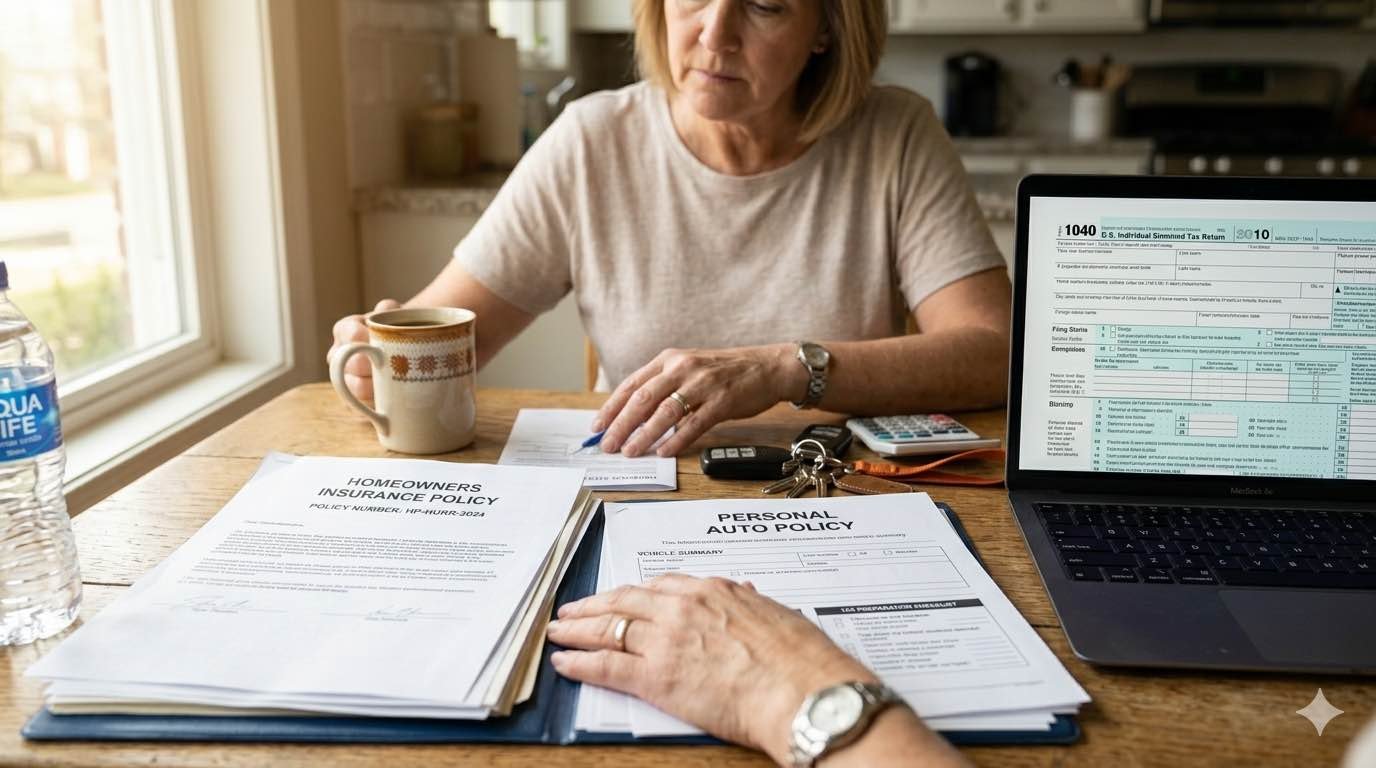

Use your tax refund to save on insurance

Okay, so maybe you don’t qualify for deductions. But if you’re expecting a tax refund, there’s a strategy almost nobody takes advantage of: paying your auto insurance premium in one shot.

The annual payment discount

Most insurers offer a 5% to 10% discount when you pay your full premium upfront instead of monthly. It might not sound like much, but let’s do the math.

If your monthly premium is $200, you pay $2,400 per year. With an 8% discount for annual payment, you save $192. It’s not a fortune, but it’s money that stays in your pocket just by changing how you pay.

Plus, you forget about monthly payments for a whole year. Less stress, less chance of missing a payment and having your policy canceled.

Other discounts you should check

Since you’re already thinking about your finances because of taxes, take the opportunity to review if you’re getting all the discounts you deserve:

The autopay discount gives you an extra 3% to 15% just for setting up automatic payments. Paperless billing adds another 2% to 5%. If you own a home or rent and can bundle with your auto insurance, that’s another 10% to 25% in potential savings.

A client told me recently he’d been overpaying for three years because he never asked about discounts. He called his insurer, asked what discounts he qualified for, and lowered his premium by $40 a month. That’s almost $500 a year.

What to do if you can’t pay your premium due to tax expenses

Sometimes April is a rough month. Between what you owe the IRS and regular expenses, insurance can feel like an extra burden. But canceling your policy is the worst decision you can make.

Driving without insurance in Florida isn’t just illegal; it also means any accident becomes a financial catastrophe. A minor crash can cost you thousands out of pocket, and if there are injuries, we’re talking numbers that can ruin you.

If you’re tight on cash, talk to your insurance agent. There are options: temporarily adjusting coverage, changing your deductible, finding a cheaper policy, or setting up a payment plan. The important thing is not to go without coverage.

Organize your documentation now

If you use your vehicle for business and plan to deduct expenses next year, start getting organized now. You’ll need:

A business mileage log. Apps like MileIQ or Everlance do this automatically. You can also use a notebook, but let’s be honest, the app is easier.

Receipts for vehicle-related expenses if you’re going to use the actual expenses method. Save everything: gas, oil changes, repairs, insurance.

A statement from your insurer showing how much you paid in premiums during the year.

The IRS can request these documents in case of an audit, so it’s better to have them organized.

The most important point

Tax Day isn’t just about what you owe or what you’re getting back. It’s an opportunity to review your complete finances, including your auto insurance.

If you have your own business or do gig work, make sure you’re taking advantage of the deductions available to you. If not, consider using your refund to pay your annual premium and save a few hundred dollars.

And whatever happens with your taxes, don’t let financial stress lead you to cancel your insurance. The consequences are much more expensive than any monthly premium.

Want to know if you’re getting all the discounts you deserve? Schedule a free policy review. We’ll help you find savings you might not have known existed.